Determined the most active banks of Uzbekistan in the 1st quarter of 2021

The Center for Economic Research and Reform has developed a "Bank activity Index" for 31 commercial banks.

The Center for Economic Research and Reform has developed a "Bank activity Index" for 31 commercial banks. The main purpose was oriented to assess constantly the changes in the share of private banks in the bank's assets, as well as the effectiveness of ongoing reforms and transformation processes in the banking sector. Based on this index, the Center publishes a rating of banks on a quarterly basis.

In calculating this index, the indicators of the following areas of the banks were considered:

The study is conducted with the aim of regularly evaluating changes in the share of the private sector in banking assets.

It is expected that the process of bank transformation will meet the demand of various segments of the population for financial services, provide territorial coverage of banking services and contribute to the implementation of socio-economic programs.

It should be noted that in 2018 more than 4 thousand individuals used remote banking services and as of January 1, 2021, their number reached almost 14 thousand, which indicates a significant increase in the coverage of digital technologies in the banking sector.

As of January 1, 2021, the assets of the banking system of the republic amounted to 366.2 trillion soums, liabilities reached to 306.6 trillion soums and capital of 59.5 trillion soums. Currently, more than 55 thousand people are work in the banking system.

Given the specific characteristics of banks, they were divided into two groups:

1) large banks 2) small banks. A particular rating was created for each group.

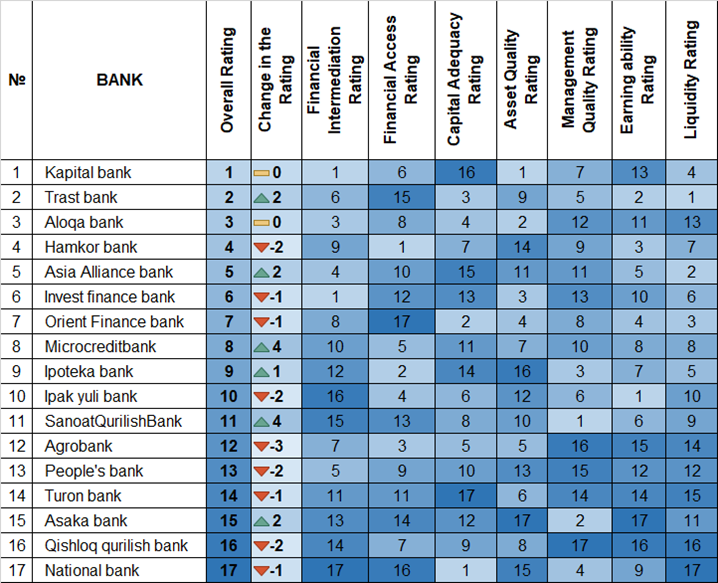

Large banks’ activity index for the 1st quarter of 2021

Among 17 major banks “Kapital Bank” leading in the overall ranking of the activity index. Kapital Bank's high results in terms of financial intermediation, asset quality and liquidity ensured the bank's 1st place. In particular, the ratio of time deposits of the bank to total loans amounted to 78%. In addition, the bank's liabilities include the share of funds received from other banks and financial institutions (3.5%) and the share of funds received from the government (1.3%).

“Trustbank” moved up 2 positions in the overall rating compared to the 4th quarter of 2020 and took 2nd place in the rating. Thus, this bank is becoming one of the leading banks in terms of capital adequacy, quality of management, profitability and liquidity. In particular, the liquidity coverage ratio is 5.2 times higher than the norm set by the CBU.

“Aloqabank” reserved its 3rd place in the overall rating as one of the largest banks with a state share. This bank performed well in financial intermediation, capital adequacy and asset quality.

The share of the bank's term deposits in the total volume of loans amounted to 56%, which is higher than other banks with the participation of the state share. At the same time, the share of deposits and loans from other banks and financial institutions in the total liabilities of Alokabank was 26%, and the share of borrowings from the state was 11%, which is lower than the average indicators (17%) of the banking system.

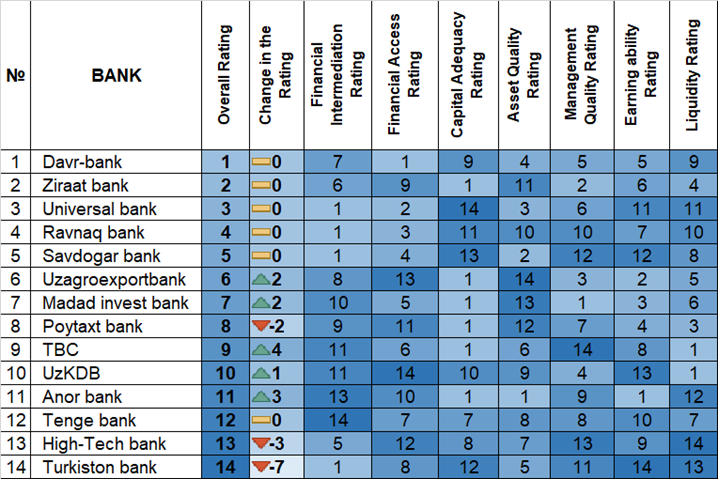

Small Banks’ Activity Index for the 1st quarter of 2021

Three leaders in the overall activity rating among 14 small banks in the first quarter of this year remained unchanged compared to 2020. The index was topped by Davrbank, Ziraatbank and Universalbank, respectively.

In terms of financial affordability, Davrbank and Universal Bank showed the highest results. Ziraatbank has become one of the leaders in terms of capital adequacy and quality of management.

A detailed analysis will be published in the next issue of the journal “Economic review”.

Tel: (+998) 78 150-02-02

e-mail: k.khamidov@cerr.uz

Kh.S. Khamidov, Lead Research Fellow, Center for Economic Research and Reform

leave a comment