"On the back of a solid reform agenda Uzbekistan established itself in somewhat exaggerated terms as "Poland" of Central Asia. The country consistently outperformed on the economic growth front and managed to avoid an outright recession in 2020 in the context of the COVID-19 crisis (as Poland did during the Global Financial Crisis)" says in their analytic article Researchers of Raiffeisen Research Center.

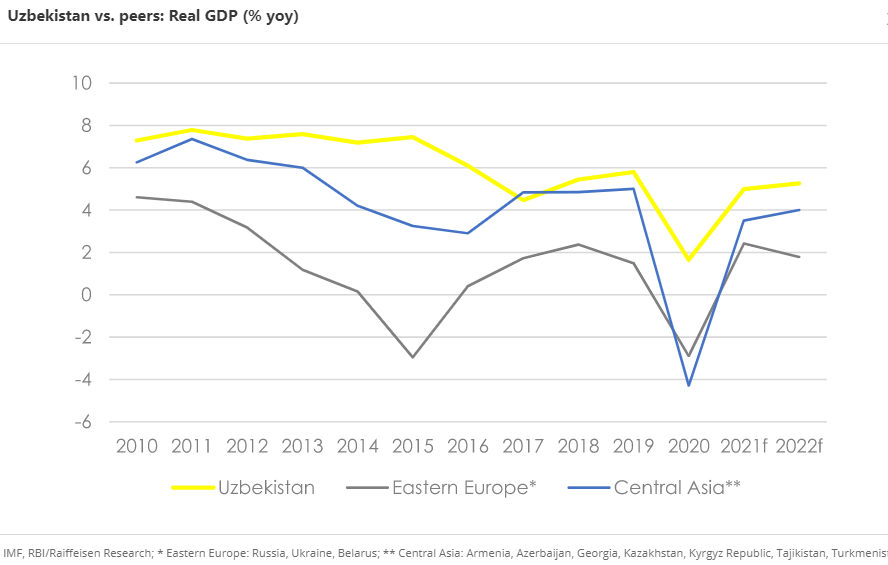

Uzbekistan: Avg. growth at 4.7% vs. 2.5% in Eastern Europe/Central Asia

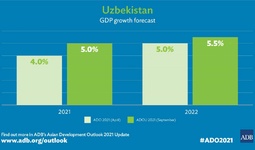

Through the cycle and incl. the COVID-19 crisis years GDP growth in Uzbekistan is likely to average ~5% 2016-2022f (vs. 2.5% in the rest of Eastern Europe/Central Asia). Such (out-)performance is usually the result of long-term sound economic policies, accumulated resilience, effective crisis management and some specifics of GDP measurement. Of course, Uzbekistan benefited from the fact that in 2020 imports slumped more than exports, which are traditionally more resilient, thus supporting the external contribution to GDP. However, the Corona crisis is also well under control. According to international statistics, we currently count ~94,000 accumulated COVID-19 cases vs. 600.000 in Central Asia on average. Currently, there are no explosive dynamics in COVID-19 cases. Therefore, the limited vaccination rate is possibly less of a risk factor than elsewhere.

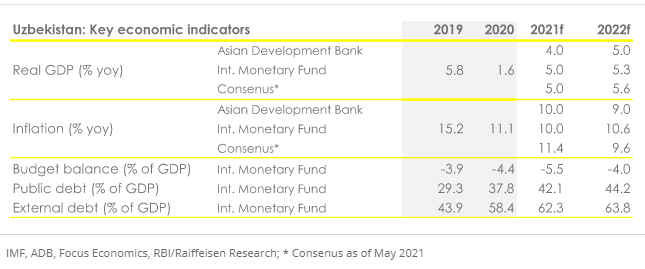

Moreover, given stability-oriented fiscal policy of recent years, authorities had been now in a position to counteract the crisis in a meaningful way without boosting the public debt-to-GDP ratio substantially above 40% of GDP. In this respect, the growth prospects are also intact. All relevant forecasters indicate GDP growth in the range of 5-6% for 2021 and 2022 — although the so-called "rebound effects" in GDP accounts will be less pronounced in Uzbekistan than in some recession economies and neighboring countries.

First phases of institutional transformation reforms underway: focus areas monetary policy and banking

The successful economic performance of recent years and the positive outlook are based on a resolute economic reform course which has been consistently pursued since 2016/2017. If this course is continued, as we expect, the considerable growth and convergence potential in the country could be further tapped. Uzbekistan currently accounts for around 1% of economic output in the CEE region, with a population share at around 7%!

In addition to long-term institutional reforms, the establishment of an independent central bank in monetary policy and banking supervision, as well as the creation of an efficient banking sector, are important (first) milestones or the foundation layer along a successful long-term economic transformation. In our core CEE region, Ukraine can be considered a prime example here, and we also see Uzbekistan well on track. Since 2019, there has been a corresponding central bank law (with a focus on central bank independence) and also a clear roadmap towards a monetary policy regime of inflation targeting (with an CPI target of 5% to be reached in 2023). From current inflation levels, there is still a long way to go, with inflation rates remaining stuck in the double digits. In this respect, it is reasonable that the Central Bank of Uzbekistan (CBU) is currently continuing to pursue a conservative or restrictive high interest rate policy, which is considerable by regional standards. This is how you position yourself as an independent economic policy player. And this is precisely where the central bank of Ukraine can be a good role model.

The key interest rate should remain well above 10% in 2021 and 2022. In addition to containing inflation and the strong lending cycle, this will also flank the opening of the local capital market to foreign investors well and at the same time may help to avoid strong currency fluctuations — even if a moderate trend currency devaluation can hardly be avoided in light of high inflation differentials.

Ultimately, Uzbekistan needs continuous capital inflows on the reform path it has embarked on and intact investor confidence to sustainably finance the investments and current account deficit expected in such a process. But the country is also well-prepared for any hick-ups during its transformation journey, with gold (!) and foreign exchange reserves amounting to about USD 33 bn, or roughly 60% of GDP, with 16-20 months of import cover. For comparison: Russia's famous and substantial foreign exchange reserves are just over 40% of GDP and 25-27 months of import coverage, while Ukraine stands at 15-20% of GDP (6 months of import coverage).

Foreign economic actors & investors participate in the growth & reform story

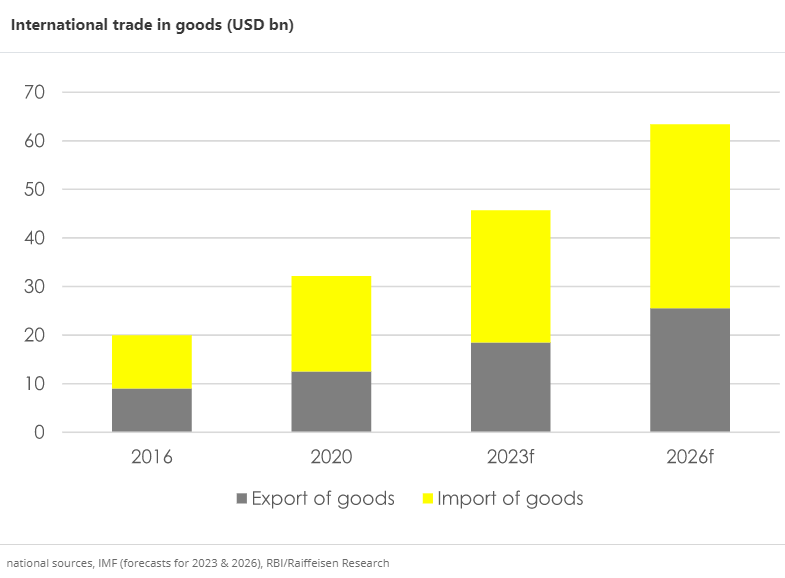

Uzbekistan's foreign trade has developed very dynamically in recent years. Foreign trade volumes (in foreign currency terms) increased by 40% over the last 5 years (from 2016-2020), import volumes have nearly doubled. In the long term, there is further strong growth potential here, with an overall trade openness (currently at ~70% of GDP) still in moderate territories in international comparison and in relation to other transition economies. Therefore, foreign trade volumes have the potential to double again by 2026.

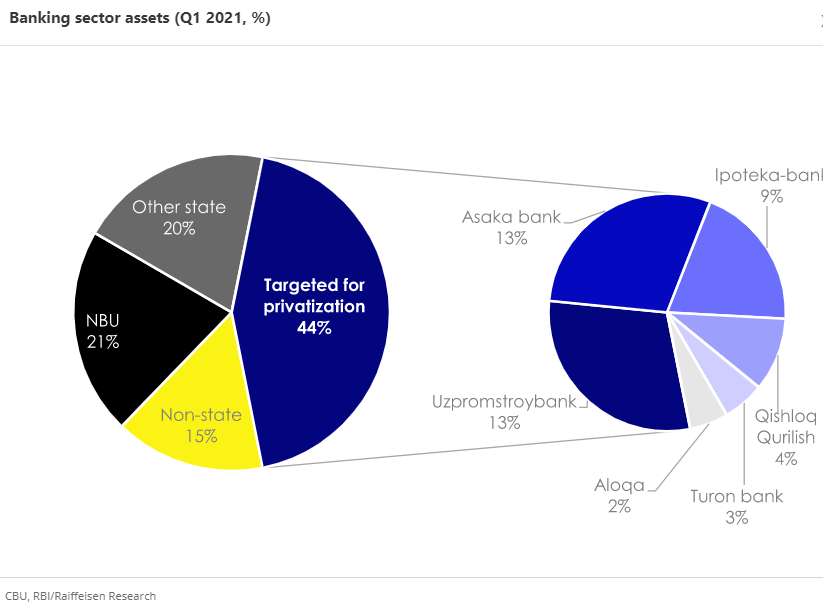

After the first successful transformations in the area of monetary and currency policy, far-reaching transformations in the banking sector are now imminent. The largely government-controlled banking system of Uzbekistan is on a quest for a new business model where the historically prevailing low-margin policy lending is replaced by market-based commercial banking. Behind this, there is also an effort to improve corporate governance, underwriting standards and efficiency ultimately preparing the sector to open up for foreign capital. In May 2020, the President of Uzbekistan approved the plan to gradually (till end-2025) reduce state participation in the banking sector from the current 85% to 40% by total assets, seeking to attract (international) strategic investors.

Importantly, the government stays there to back the sector’s revamp, in turn securing advisory and financial assistance of multilateral financial organizations that support Uzbekistan’s wider reforms agenda. The targeted transformation is likely to intensify competition among banks, though this is for the moment mitigated by the general expansion of the banking industry which is affordable in the context of still moderate credit penetration and financial intermediation levels (total banking assets at 60% of GDP). Moreover, the transition towards an open market, price stability and private sector development should enhance credit intermediation in local currency, promising a decline in loans dollarization in the longer-run (2020: ~50% of the total portfolio, but absent in retail loans).

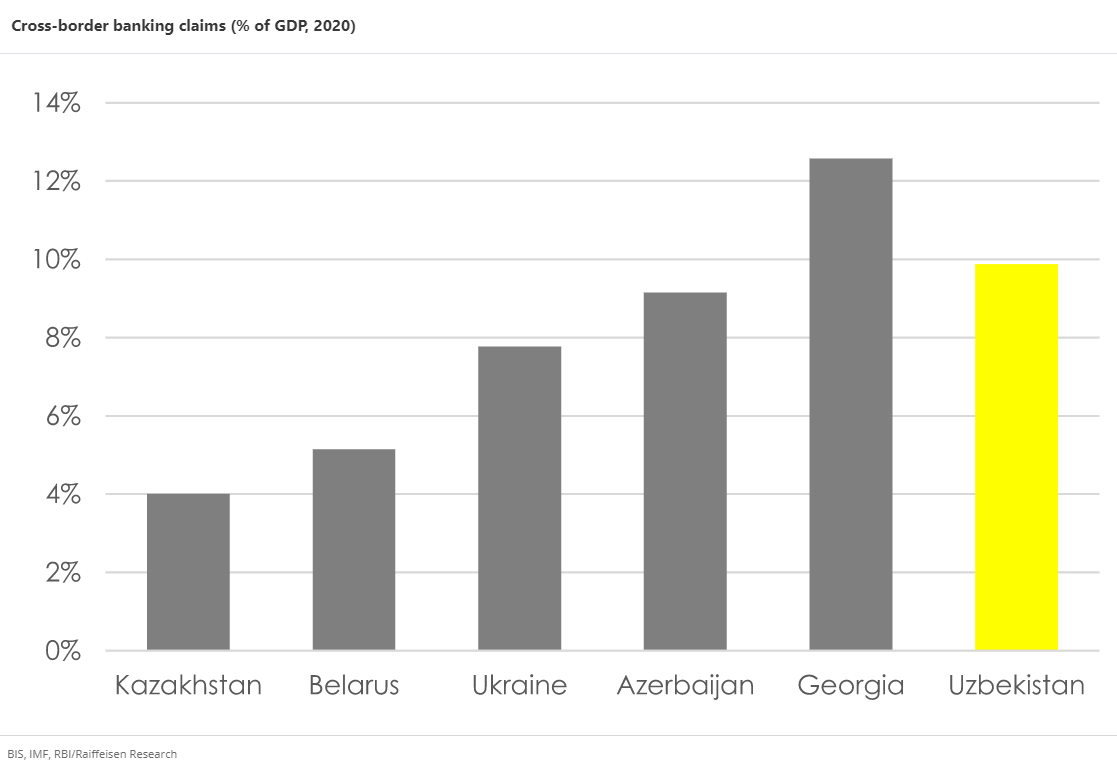

Exposures of international banks increase strongly; but not yet exuberant

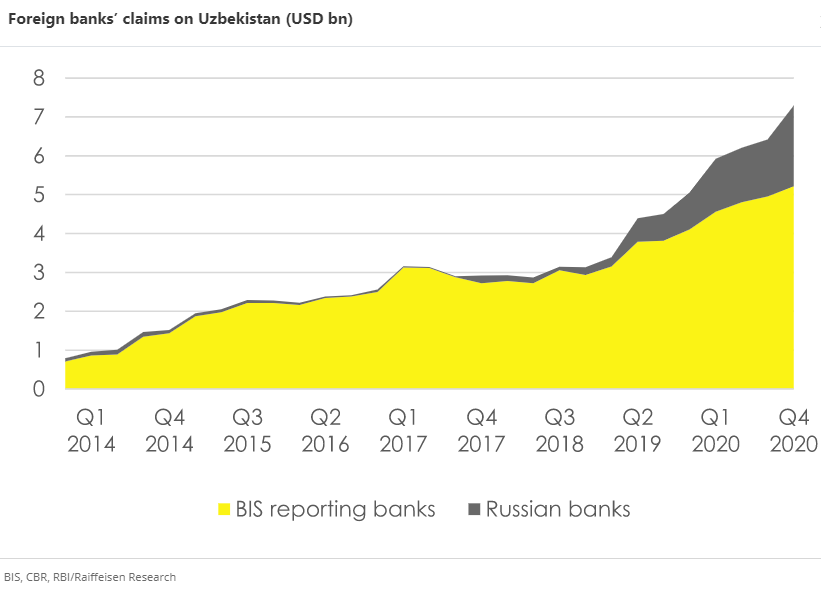

The invite for foreign capital in the banking sector resonates well with the generally growing appetite for Uzbek risk by international investors. Foreign banks have unmistakably increased their exposures towards Uzbekistan significantly in recent years. Apart from the successful Eurobond placings worth nearly USD 3 bn in 2019-2021 year-to-date (sovereign, banks and corporates), there has been a steep rise in cross-border banking claims on Uzbekistan by both BIS-reporting and Russian lenders, up to USD 7 bn together (more than 2 times up since 2018). In this regard, the steady inflow of wholesale funding mitigates still rather narrow local deposit base of Uzbek banks (the sector’s Loan-to-deposit ratio stands at ~250%). In the long term, the trend of exposure increases at foreign banks is even more impressive. Western banks have increased their exposures towards Uzbekistan by a factor of 6-7 increased from just under USD 1 billion in 2012 to almost USD 6 billion by the end of 2020. While this momentum cannot continue indefinitely, it is not yet in exuberant territory. In the case of unsustainable expansion strategies in CEE frontier markets, Western banks, for example, had increased their exposures to Kazakhstan or Ukraine by a factor of 30 to 60 from 2000-2007/2008 (from similarly low starting levels as in the case of Uzbekistan).

Uzbekistan: Cross-border banking claims: Over time and vs. peers

Authors:

Gunter Deuber is heading the Economics and Financial Analysis division (Raiffeisen Research) at Raiffeisen Bank International (RBI).

Ruslan Gadeev is a Senior Financial Analyst in the Fixed Income team at Raiffeisen Research covering banking markets in the CEE space.

leave a comment