Uzbekistan’s Banking Sector in the CERR Ranking

The Center for Economic Research and Reforms (CERR) has released an updated Bank Activity Index Ranking for the Q3 2025.

The updated ranking confirms the gradual strengthening of the stability of Uzbekistan’s banking sector. Major players continue to hold leading positions, relying on their extensive branch networks across the country, diversified assets, and a stable client base. At the same time, a noticeable reshuffling has taken place in the mid-tier segment.

The study covers 35 commercial banks in the country, of which 20 are classified as large financial institutions based on their scale and branch network, and 15 are categorized as small banks.

The methodology is based on the analysis of 27 indicators compared against national averages and international standards, including the requirements of the Basel Committee. This approach ensures an objective assessment of the current state of the banking sector and allows monitoring of its dynamics over time.

The ranking serves as an important tool to enhance transparency and strengthen confidence in the financial system. Its regular updates stimulate competition among banks and contribute to improving the quality of services. This approach aligns with international practice and is applied by leading financial institutions worldwide.

Financial results for the Q3 2025

During the reporting period, the total assets of the banking sector amounted to 863 trillion sums ($71.2 billion), while liabilities reached 734 trillion sums ($60.6 billion). A moderate slowdown in lending was observed, down to 14%, while deposit growth remained strong at around 28%. The share of foreign currency operations declined, indicating the strengthening role of the national currency. Net profit reached 9 trillion sums, up by one quarter from the previous year, and return on equity rose to 11.2%. The sector demonstrates adaptability, continuing to support the economy amid shifting market conditions.

The share of non-performing loans (NPLs) fell to 3.8%, down from 4.2% a year earlier, indicating an improvement in portfolio quality, though in some banks this indicator remains above the average. Capital adequacy ratios exceed the minimum regulatory requirements by more than 1.3 times, confirming the sector’s resilience.

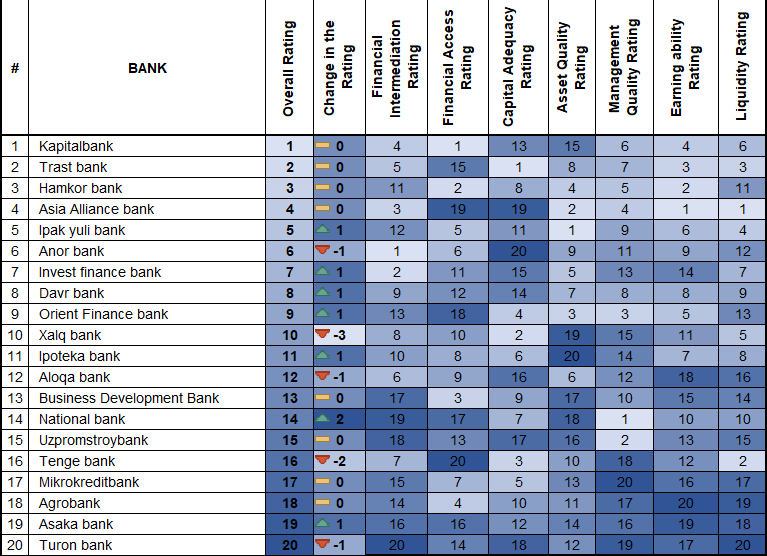

Activity ranking of large banks for Q3 2025

The Q3 2025 activity ranking of large banks showed that sector leaders maintained their strong positions. The top four – Kapitalbank, Trastbank, Hamkorbank, and Asia Alliance Bank – retained their places in the overall ranking, confirming their competitive advantages through extensive branch networks, diversified portfolios, and strong customer bases.

Significant changes were observed in the mid-tier segment. Ipak Yuli Bank entered the top five, improving its performance, while Infinbank, Davrbank, Orient Finance Bank, Ipoteka Bank, and Asaka Bank all strengthened their positions. The greatest progress was demonstrated by the National Bank, which rose by two places in the overall ranking.

At the same time, five large banks lost positions in the overall ranking, with Xalq Bank and Tenge Bank showing the most notable declines – by three and two points, respectively. Four commercial banks – BRB, Uzpromstroybank, Mikrokreditbank, and Agrobank – maintained their previous positions.

Trends in key indicators of the banking sector

Financial intermediation. Several banks demonstrated a decline in efficiency in attracting and allocating resources. Ipak Yuli Bank, Invest Finance Bank, Davrbank, Xalq Bank, Mikrokreditbank, Aloqabank, and Turonbank each improved by one position, reflecting the sensitivity of indicators to changes in the structure of deposits and liabilities.

Financial accessibility. Declines were recorded for Anor Bank (–3 points), Asaka Bank and Agrobank (–2 each), and Asia Alliance Bank, Davrbank, Uzpromstroybank, Xalq Bank, Ipoteka Bank, and Turonbank (–1 each). This trend is linked to branch load and increased credit risk concentration.

Asset quality. Ipoteka Bank remained in last place, Davrbank fell by six positions, Anor Bank by three, while Hamkorbank, Tenge Bank, and Xalq Bank each dropped by two.

Despite overall profit growth in the sector, several banks recorded declines in profitability indicators. Agrobank retained its weak position, while Hamkorbank, Anor Bank, Tenge Bank, and Turonbank each slipped by one position in this category, indicating pressure from interest expenses and limited growth in non-interest income.

Management Efficiency and Liquidity Indicators

In terms of management efficiency, weak performance was observed at Mikrokreditbank, while Aloqabank and BRB each fell by three positions. Tenge Bank, Ipoteka Bank, and Turonbank each declined by two. Additionally, several other banks slipped by one position, indicating the need to improve staff performance and optimize operational costs.

Regarding liquidity indicators, Turonbank ranked last. At the same time, Hamkorbank, Anor Bank, and Orient Finans Bank each lost three positions; Trastbank dropped by two, while Kapitalbank and Ipoteka Bank fell by one line each.

Overall, the analysis confirms the continued stability of the largest sector players amid a reshuffling within the mid-tier segment.

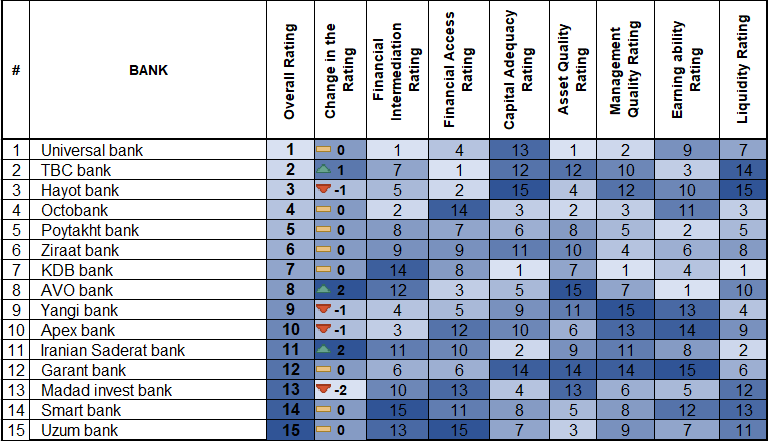

Activity Ranking of Small Banks for Q3 2025

In the group of small banks, leadership remains concentrated: the top five retained their positions thanks to strong metrics in liquidity, profitability, and asset quality. Movements within the ranking mainly occurred in the middle segment – several banks advanced by 1–2 positions due to stronger financial intermediation and growth in non-interest income, while others fell because of declining efficiency and narrowing profit margins.

Among small banks, 8 out of 15 institutions, including the group leader Universal Bank, maintained their positions. Meanwhile, four banks experienced declines, the largest being Madad Invest Bank, which fell by two places. In contrast, Saderat Bank Iran and AVO Bank each rose by two positions, while TBC Bank gained one position, securing second place overall in the group ranking.

According to the results, banks in this group that actively attract deposits while remaining less dependent on borrowings tend to demonstrate stronger performance. Institutions that provide broader access to services and maintain a more balanced distribution of loans also show more stable positions.

Losses in the ranking were mainly associated with a rise in non-performing loans, while banks with cleaner portfolios retained top positions. Profitability was positively influenced by diversified income sources and effective cost control. Overall, the sector’s liquidity remains stable.

Banking and Financial Sector Research Sector

Tel: (78) 150 02 02 (441)

Public Relations and Media Sector

Tel: (78) 150 02 02 (417)

leave a comment