The Center for Economic Research and Reforms presented its updated Bank Ranking based on the results of the Bank Activity Index for Q2 2026.

The study covers 34 commercial banks operating in Uzbekistan. To ensure comparability, 20 banks were classified as large banks and 14 as small banks.

The Index is calculated using 27 sub-indicators grouped into eight areas, including financial intermediation, financial accessibility, capital adequacy, asset quality, management efficiency, profitability, and liquidity.

The indicators are compared with banking system averages and applicable international standards, including the requirements of the Basel Committee on Banking Supervision.

This approach is consistent with international practice and is used by leading financial institutions.

Financial Results for Q2 2026

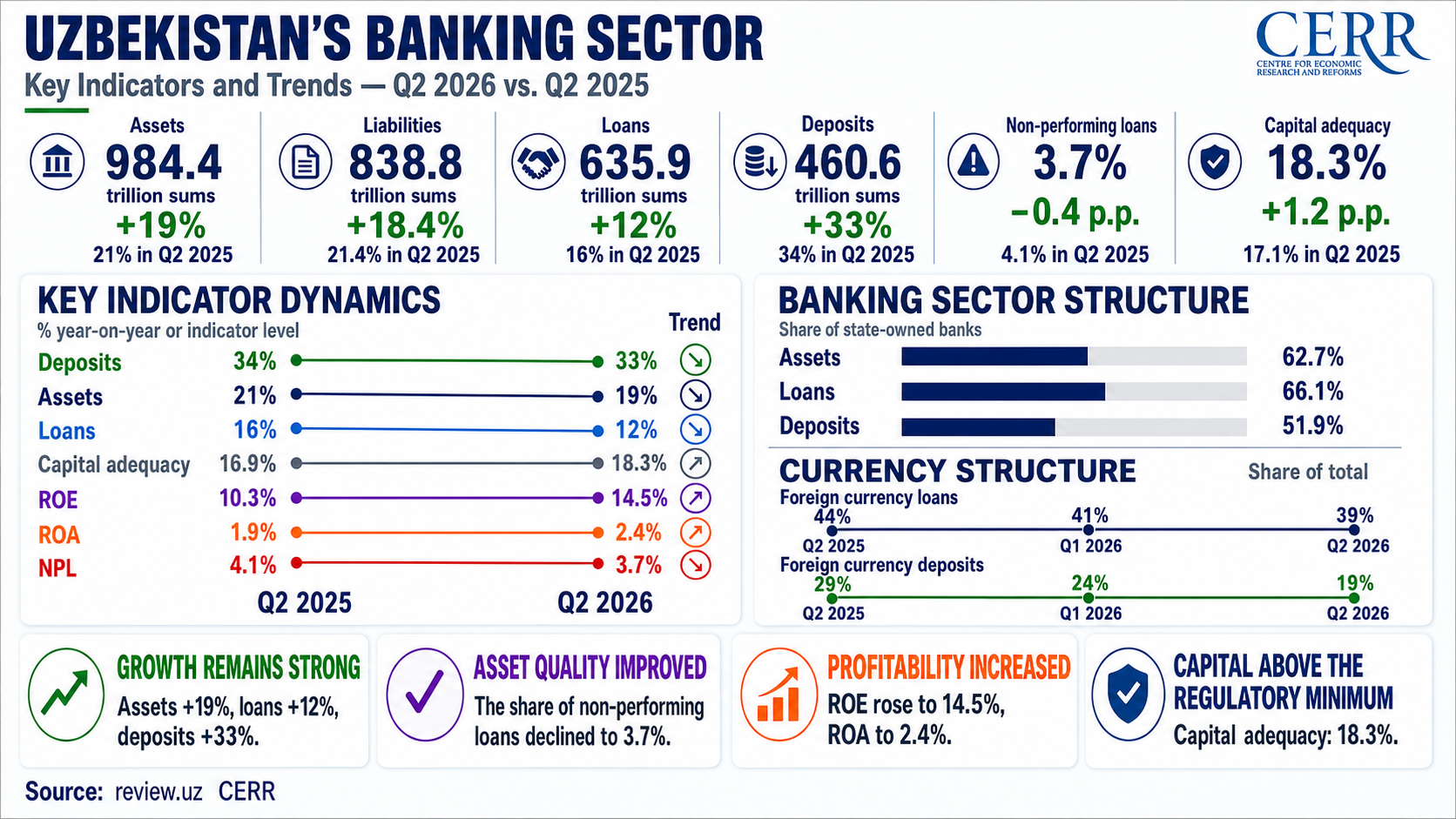

Asset Growth Continues

As of June 1, 2026, total banking system assets reached 984.4 trillion sums, up 19% year over year. Liabilities increased by 18.4% to 838.8 trillion sums. The market structure remained largely unchanged. Nine state-owned banks accounted for 62.7% of total assets and 66.1% of the loan portfolio.

Deposit Growth Outpaces Lending

Deposits continued to grow significantly faster than lending. Over the year, outstanding loans increased by 12%, while deposits rose by 33%, strengthening the banking system and supporting high liquidity levels.

Private banks continued to demonstrate higher deposit coverage of their loan portfolios. State-owned banks held 57 sums in deposits for every 100 sums in loans, compared with 103 sums at private banks. This indicates that state-owned banks remain more dependent on other funding sources.

Profitability and Liquidity Improved

The banking sector’s financial performance strengthened considerably. Net profit rose by 66.7% to 8.5 trillion sums. The main contribution came from a 2.5-fold increase in the non-interest margin, which reached 15.8 trillion sums.

Against this backdrop, return on assets (ROA) increased from 1.9% to 2.4%, while return on equity (ROE) rose from 10.3% to 14.5%. At the same time, the share of highly liquid assets increased by 4.2 percentage points to 21.6%.

Asset Quality Improved, but Some Risks Remain

The non-performing loan ratio declined from 4.1% to 3.7%, indicating an improvement in loan portfolio quality. However, NPL ratios remained relatively high at some state-owned and private banks.

The dollarization of banking operations continued to decline. The share of foreign currency loans decreased from 41% to 39%, while the share of foreign currency deposits fell from 24% to 19%. Capital adequacy ratios remained approximately 1.5 times above the minimum requirements.

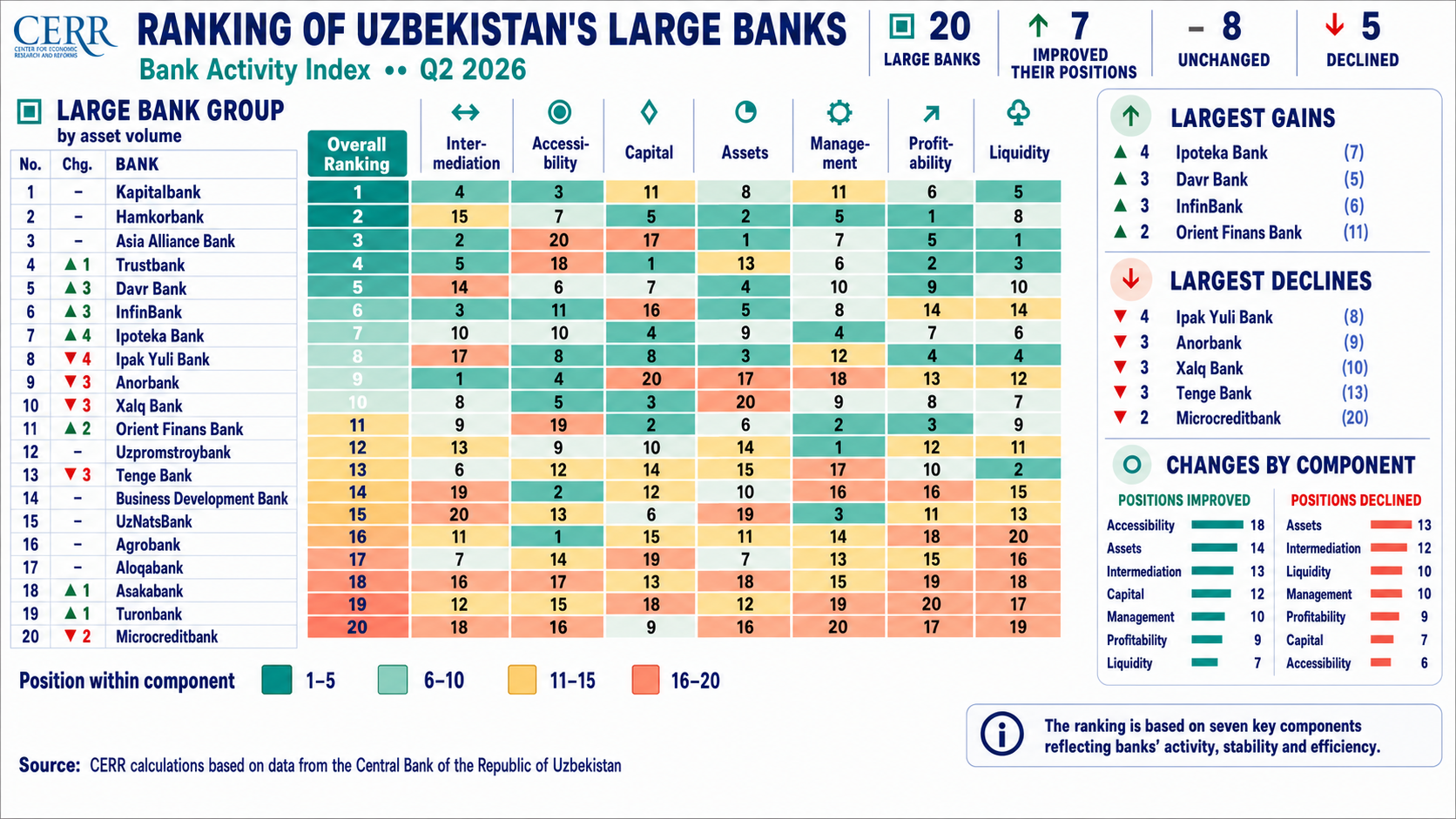

Large Bank Activity Ranking for Q2 2026

Changes in the Ranking

In Q2 2026, the positions of 12 of the 20 large banks changed. Seven banks improved their rankings, five moved down, and eight retained their previous positions. Ranking movements were driven by changes in individual components of the Index.

Financial accessibility made the largest positive contribution, while asset quality and liquidity constrained the advancement of some banks. The top three positions remained unchanged, with most movements occurring in the lower two-thirds of the ranking.

Key Changes by Index Component

Positive dynamics were primarily recorded in financial accessibility, asset quality, financial intermediation, and capital adequacy. At the same time, some banks lost ground in asset quality, liquidity, and management efficiency. The most significant changes by component were as follows.

In financial accessibility, 12 large banks improved their positions, while four moved down. Hamkorbank, InfinBank, Uzpromstroybank, and Turonbank recorded the largest gains, each moving up two positions. Mikrokreditbank posted the sharpest decline, falling by 11 positions.

In financial intermediation, seven large banks improved their positions, while nine declined. Orient Finans Bank made a significant leap, rising by 10 positions. Turonbank moved up five positions. Mikrokreditbank recorded the largest decline in activity, falling by 10 positions.

In asset quality, nine large banks strengthened their positions, while the same number failed to retain their previous rankings. Ipoteka Bank recorded the strongest improvement, rising by seven positions, while Uzpromstroybank moved up three positions. Tenge Bank fell by five positions, and Anorbank declined by four.

In capital adequacy, eight large banks demonstrated positive dynamics, while nine retained their positions. Davr Bank and Ipoteka Bank recorded the largest improvements, each rising by three positions. Tenge Bank posted a significant decline, falling by 10 positions.

In management efficiency, seven large banks improved their positions, while the same number moved down. Ipoteka Bank showed the strongest positive dynamics, rising by seven positions. Tenge Bank recorded a pronounced decline of seven positions, followed by InfinBank with a four-position drop and Davr Bank with a three-position decline.

Profitability results were distributed almost evenly. Five large banks improved their positions, five declined, and another 10 remained unchanged. Orient Finans Bank posted the largest gain, moving up two positions. Asia Alliance Bank recorded the most notable decline, falling by two positions.

In liquidity, three large banks improved their positions, while six declined. Orient Finans Bank recorded the strongest increase, rising by nine positions, while Tenge Bank improved by three positions. Asakabank fell by five positions, the National Bank of Uzbekistan by three positions, and Ipak Yuli Bank by two positions.

Bank Activity Dynamics

The top three positions among large banks remained unchanged. Kapitalbank ranked first, followed by Hamkorbank in second place and Asia Alliance Bank in third.

Ipoteka Bank recorded the strongest positive movement in the overall ranking, rising by four positions to seventh place. This improvement was supported by stronger asset quality, capital adequacy, and management efficiency indicators.

Davr Bank and InfinBank followed, each moving up three positions. Davr Bank rose to fifth place after improving its financial accessibility, asset quality, capital adequacy, and profitability indicators. InfinBank took sixth place, supported by strong results in financial accessibility, capital adequacy, and asset quality.

Ipak Yuli Bank recorded a notable decline in Q2, falling by four positions to eighth place in the overall ranking. This was driven by weaker financial intermediation and liquidity indicators.

Anorbank, Xalq Bank, and Tenge Bank also stood out in terms of declining activity, each losing three positions in the overall ranking.

Anorbank ranked ninth following weaker financial accessibility, asset quality, management efficiency, and profitability indicators. Xalq Bank moved to 10th place due to declines in asset quality, management efficiency, and profitability. Tenge Bank ranked 13th, reflecting weaker capital adequacy, management efficiency, and asset quality.

Transformation Processes

Asset quality, liquidity, financial intermediation, and management efficiency remain constraining factors for some banks.

While financial accessibility and capital adequacy continue to improve, banks’ ability to strengthen their positions will depend on asset quality, profitability, risk management, and the sustainability of their operating results.

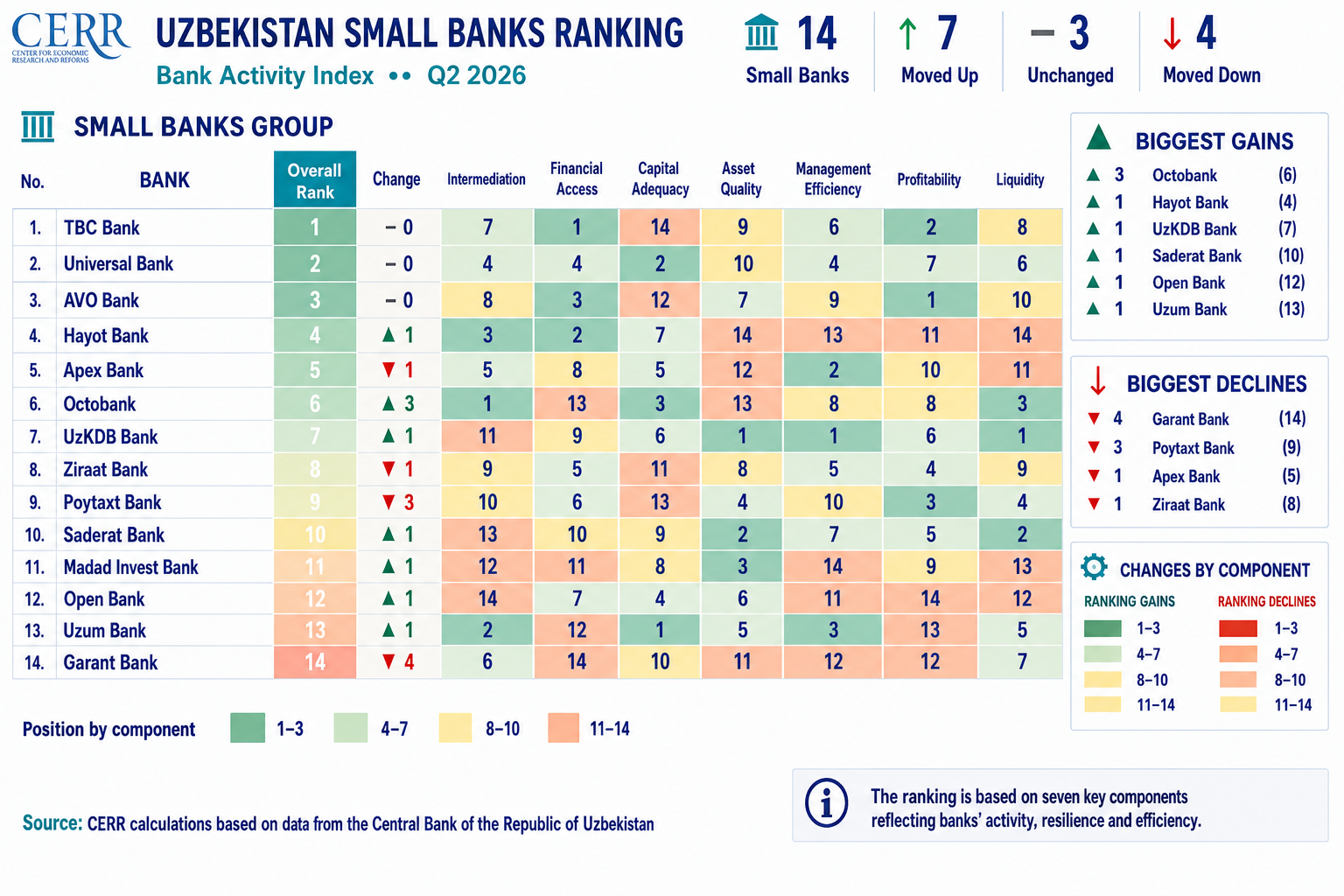

Small Bank Activity Ranking for Q2 2026

As in the large-bank ranking, the top three positions among small banks remained unchanged. TBC Bank ranked first, Universal Bank second, and AVO Bank third.

Octobank recorded the strongest positive movement in the overall ranking, rising by three positions to sixth place. The improvement was driven by stronger profitability, management efficiency, and financial accessibility indicators.

Hayot Bank, UzKDB Bank, Saderat Bank, Madad Invest Bank, Open Bank, and Uzum Bank each moved up one position. Their improved rankings were supported by gains in individual Index components, particularly financial accessibility, asset quality, liquidity, and capital adequacy.

Garant Bank posted a notable decline in the overall ranking, falling by four positions to 14th place. This was associated with weaker financial accessibility, asset quality, and liquidity indicators.

Poytaxt Bank recorded the next-largest decline, losing three positions and ranking ninth. Apex Bank and Ziraat Bank each moved down one position due to changes in individual components of the Index.

Jafar Khidirov

CERR Banking and Financial Sector Research Sector

Tel.: (78) 150-02-02, ext. 441

CERR Public Relations and Media Sector

Tel.: (78) 150-02-02, ext. 417

leave a comment