According to World Bank estimates, Uzbekistan’s GDP grew by 6.2% in 2021

According to the latest edition of the World Bank's «World Economic Prospects» report, GDP of Uzbekistan grew by 6.2%.

The rapid spread of the Omicron variant indicates that the pandemic will likely continue to disrupt economic activity in the near term.

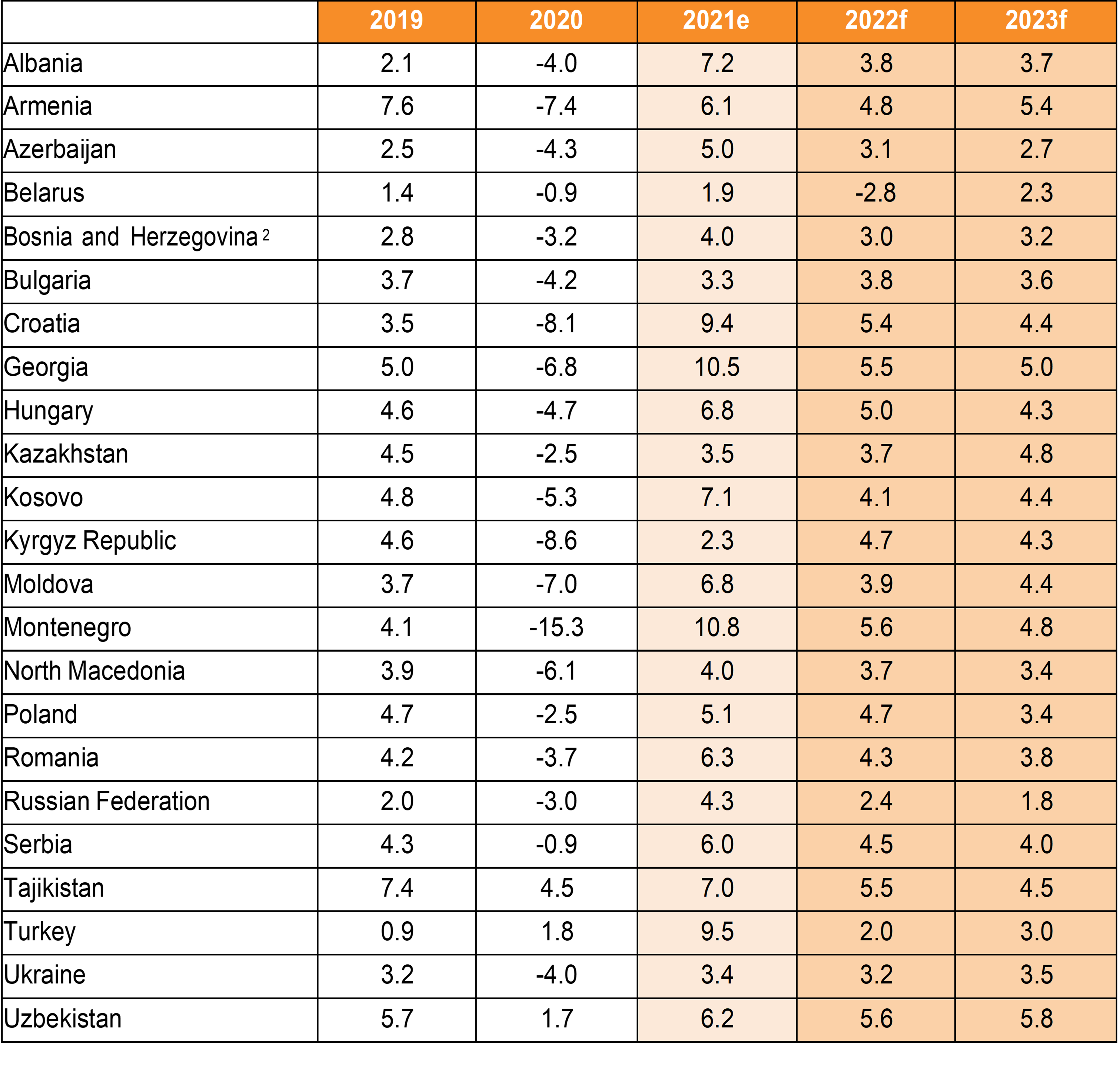

In 2021, GDP growth in Uzbekistan reached 6.2%, while Tajikistan and Kazakhstan recorded 7.1% and 3.5% respectively. The World Bank predicts that Uzbekistan's GDP will grow the most in Central Asia in 2022 and 2023. It is predicted that the growth of the national economy of Uzbekistan in 2022 and 2023 will be 5.6% and 5.8%, respectively.

Europe and Central Asia country forecasts 1

(Real GDP growth at market prices in percent, unless indicated otherwise)

Source: World Bank.

Source: World Bank.

Following a strong rebound in 2021, the global economy is entering a pronounced slowdown amid fresh threats from COVID-19 variants and a rise in inflation, debt, and income inequality that could endanger the recovery in emerging and developing economies, according to the World Bank’s latest Global Economic Prospects report. Global growth is expected to decelerate markedly from 5.5 percent in 2021 to 4.1 percent in 2022 and 3.2 percent in 2023 as pent-up demand dissipates and as fiscal and monetary support is unwound across the world.

At a time when governments in many developing economies lack the policy space to support activity if needed, new COVID-19 outbreaks, persistent supply-chain bottlenecks and inflationary pressures, and elevated financial vulnerabilities in large swaths of the world could increase the risk of a hard landing.

“The world economy is simultaneously facing COVID-19, inflation, and policy uncertainty, with government spending and monetary policies in uncharted territory. Rising inequality and security challenges are particularly harmful for developing countries,” said World Bank Group President David Malpass. “Putting more countries on a favorable growth path requires concerted international action and a comprehensive set of national policy responses.”

The slowdown will coincide with a widening divergence in growth rates between advanced economies and emerging and developing economies. Growth in advanced economies is expected to decline from 5 percent in 2021 to 3.8 percent in 2022 and 2.3 percent in 2023—a pace that, while moderating, will be sufficient to restore output and investment to their pre-pandemic trend in these economies. In emerging and developing economies, however, growth is expected to drop from 6.3 percent in 2021 to 4.6 percent in 2022 and 4.4 percent in 2023. By 2023, all advanced economies will have achieved a full output recovery; yet output in emerging and developing economies will remain 4 percent below its pre-pandemic trend. For many vulnerable economies, the setback is even larger: output of fragile and conflict-affected economies will be 7.5 percent below its pre-pandemic trend, and output of small island states will be 8.5 percent below.

Output in Europe and Central Asia (ECA) is estimated to have expanded by 5.8 percent in 2021, reflecting a rebound in domestic demand and positive spillovers from firming activity in the euro area. Growth is forecast to slow to 3 percent in 2022, as domestic demand stabilizes, and 2.9 percent in 2023, as external demand plateaus and commodity prices soften. The near-term outlook is weaker than previously projected, owing to recurrent COVID-19 flareups, a faster-than-expected withdrawal of macroeconomic policy support, and sharp increases in policy uncertainty and geopolitical tensions. The pace of growth over the forecast horizon will leave output slightly lower than its pre-pandemic trend by 2023, and the catch-up of per capita income growth with advanced economies will be slower during 2021-23 than in the decade before the pandemic. Key risks to the regional outlook include a further resurgence of the pandemic, financial stress, less supportive external conditions than expected, and an additional rise in policy uncertainty or escalation in geopolitical tensions.

leave a comment