Intra-regional Trade in Central Asia in Q1 2026

CERR has prepared an infographic on the dynamics of intra-regional trade among Central Asian countries in Q1 2026.

In Q1 2026, intra-regional trade in Central Asia showed a noticeable acceleration. The total volume of mutual trade among the countries of the region reached $3.2 bn, increasing by 29.0% compared with the same period last year.

Almost all countries of the region, with the exception of Kyrgyzstan, significantly increased supplies to Central Asian countries: Kazakhstan by 30%, Tajikistan by 36%, Turkmenistan by 79%, and Uzbekistan by 19%.

This dynamic shows that amid heightened global turbulence, the regional market continues to be of high importance for Central Asian countries and is becoming one of the factors supporting foreign trade activity.

Kazakhstan accounted for 60.2% of total mutual exports among Central Asian countries, Uzbekistan for 20.1%, Turkmenistan for 11.8%, Kyrgyzstan for 5.5%, and Tajikistan for 2.4%. Thus, more than 80% of regional trade is concentrated in the two largest economies of Central Asia — Kazakhstan and Uzbekistan.

At the same time, a pronounced asymmetry in trade balances remains. Kazakhstan maintains a stable export surplus in trade with neighbouring countries. Uzbekistan is increasing trade with the region, but this growth is largely driven by higher imports from Kazakhstan and Turkmenistan. Kyrgyzstan and Tajikistan remain more dependent on regional imports than on exports to neighbouring countries.

Overall, intra-regional trade in Central Asia is developing along an upward trajectory, although its structure remains concentrated and uneven.

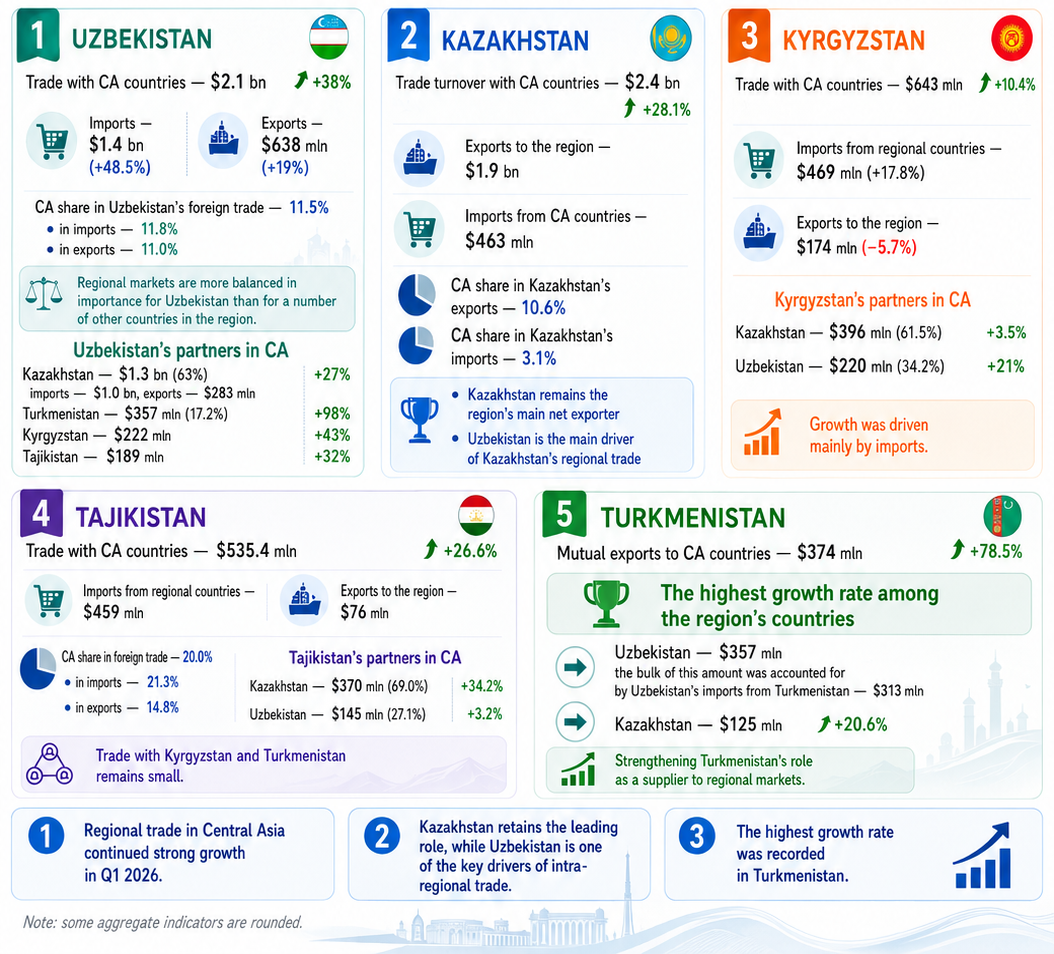

Kazakhstan retains its status as the largest participant in intra-regional trade. Its trade turnover with Central Asian countries in Q1 2026 amounted to $2.4 bn, increasing by 28.1%.

Kazakhstan’s exports to the region reached $1.9 bn, while imports from Central Asian countries amounted to $463 mn.

Kazakhstan remains the region’s main net exporter, while regional markets serve as a major sales destination. Central Asia accounts for 10.6% of Kazakhstan’s exports, but only 3.1% of its imports.

By country, Kazakhstan increased trade volumes with all countries of the region. In particular, trade with Uzbekistan grew by 34.9%, reaching $1.3 bn, or 56.3% of Kazakhstan’s total trade with Central Asian countries. Uzbekistan is the main driver of Kazakhstan’s regional trade. Trade also increased with Kyrgyzstan by 18.2% to $550 mn, with Tajikistan by 23.3% to $361 mn, and with Turkmenistan by 20.6% to $125 mn.

Kyrgyzstan’s trade with Central Asian countries increased by 10.4% and amounted to $643 mn. However, this growth was mainly driven by imports: supplies from the region to Kyrgyzstan reached $469 mn, increasing by 17.8%, while Kyrgyzstan’s exports to the region declined by 5.7% to $174 mn.

It is important to note that Central Asia is particularly important for Kyrgyzstan as an export market: the region accounts for 36.1% of the country’s total exports. At the same time, the region’s share in imports is 16.3%, and in overall foreign trade — 19.2%.

By country, Kyrgyzstan’s key partners remain Kazakhstan and Uzbekistan. Kazakhstan accounts for $396 mn, or 61.5% of Kyrgyzstan’s trade with the region, with growth of 3.5%. Trade with Uzbekistan amounted to $220 mn, or 34.2%, and increased by 21%. Together, these two directions form almost all of Kyrgyzstan’s regional trade turnover. Trade with Turkmenistan declined by 20.8% to $15 mn.

It is also necessary to note the continuing trend of expanding trade with Tajikistan after the easing of tensions in bilateral relations. In Q1, trade increased 29-fold, although volumes remain relatively small at $13 mn.

In Q1 2026, Tajikistan increased trade with Central Asian countries to $535.4 mn, which is 26.6% higher than a year earlier. Imports from the region amounted to $459 mn, while exports totalled only $76 mn. The share of Central Asian countries in Tajikistan’s foreign trade reached 20%, including 21.3% in imports and 14.8% in exports.

Kazakhstan remains the main partner, accounting for $370 mn, or 69% of Tajikistan’s trade with Central Asian countries. Trade with Kazakhstan grew by 34.2%. The second major direction is Uzbekistan, with which trade turnover amounted to $145 mn, or 27.1%, with growth of 3.2%. Trade with Kyrgyzstan and Turkmenistan remains limited.

The main trend for Tajikistan is the growth of regional trade while a significant import bias persists.

According to mirror trade data, Turkmenistan’s mutual exports to Central Asian countries amounted to $374 mn, increasing by 78.5%. This is the highest growth rate among the countries of the region, indicating the strengthening of Turkmenistan’s role as a supplier to regional markets.

The most pronounced growth is observed in trade with Uzbekistan. Uzbekistan’s trade turnover with Turkmenistan reached $357 mn, almost doubling. The bulk of this volume was accounted for by Uzbekistan’s imports from Turkmenistan, which amounted to $313 mn. Turkmenistan’s trade with Kazakhstan increased by 20.6% to $125 mn. At the same time, trade volumes with Kyrgyzstan and Tajikistan remain limited.

Uzbekistan’s trade with Central Asian countries in Q1 2026 amounted to $2.1 bn, increasing by 38%. However, trade growth with neighbouring countries was driven to a greater extent by imports. Imports reached $1.4 bn, increasing by 48.5%, while exports to the region amounted to $638 mn, growing by 19%.

The share of Central Asian countries in Uzbekistan’s foreign trade amounted to 11.5%, including 11.8% in imports and 11% in exports. This shows that regional markets have a more balanced importance for Uzbekistan than for several other countries in the region, where pronounced imbalances are observed.

By country, Uzbekistan increased trade volumes with all Central Asian countries. Trade with Uzbekistan’s largest regional partner — Kazakhstan — grew by 27% and reached $1.3 bn, accounting for 63% of Uzbekistan’s trade with Central Asian countries. Imports from Kazakhstan amounted to $1 bn, while exports stood at $283 mn.

The second major direction was Turkmenistan — $357 mn, or 17.2% of Uzbekistan’s regional trade, with growth of 98%. Trade with Kyrgyzstan increased by 43% to $222 mn, while trade with Tajikistan grew by 32% to $189 mn.

The results of Q1 2026 show that intra-regional trade in Central Asia continues to strengthen amid an unstable external economic environment.

At the same time, regional trade is developing around several key centres and directions. Kazakhstan maintains its role as the largest exporter and the main supplier to neighbouring countries. Uzbekistan acts as a major import market and an active exporter in selected directions. Turkmenistan has sharply strengthened its export role, primarily due to increased supplies to Uzbekistan. Kyrgyzstan and Tajikistan remain more dependent on regional imports and concentrate their trade mainly on Kazakhstan and Uzbekistan.

Thus, in Q1 2026, Central Asia demonstrated positive momentum in mutual trade. However, the next stage of regional integration should be associated not only with growth in trade turnover, but also with improving the quality of trade and economic ties among the countries of the region.

Trade remains asymmetric and concentrated, while countries’ export capacities differ. Therefore, further strengthening of trade ties should be accompanied by the development of industrial cooperation, expansion of joint production chains, reduction of logistics barriers, and harmonisation of technical requirements.

Ruslan Abaturov, CERR

leave a comment